The primary asset of the Trust is its interest in insurance policies. The Trust owns the beneficial interest in each of them, but the actual legal owner is Advance Trust & Life Escrow Services, LTA (ATLES) which is located in Waco, Texas. ATLES receives the death benefits from each policy as they are paid by the insurance company and acts as escrow agent/securities intermediary as required under the Bankruptcy Plan. ATLES has no interest or claim to the funds. Instead, all of the death benefit proceeds are owned by the Trust as beneficiary. Set forth below is more information regarding the policies.

The Number and Type of Policies

As of June 30, 2022, the Trust owns an interest in a total of 2,435 policies. There are 330 life settlements and 2,105 viaticals.

Life settlements are generally insurance policies issued with respect to a person who was elderly at the time Life Partners acquired the policy. Generally, they have no health issues other than being old. However, when you invested you were told the person only had a short time to live which was a bunch of nonsense and was the essence of the fraud in the entire program run by Life Partners. Years later many of these people are still alive and are now in their mid to late 90s. The face amount of these policies is usually several million dollars and the premiums rise each year as the person grows older. Once they get to their mid to late 90s the premiums rise very rapidly and that is why you see increases in the amount of your premium bill each year. Expect the amount of your premium bill to keep going up each year.

Viaticals on the other hand are generally policies issued with respect to a person who had a life-threatening illness at the time Life Partners acquired the policies. In most instances, that illness was HIV and the insureds were not expected to live very long. Again, when you invested you were told they would die very shortly and that was also not accurate. With the advancement of medicine relating to the HIV virus, the vast majority of the insureds survived and are still alive now many years later. These policies generally have a small face amount and the premiums generally stay level throughout the term of the policy. So, the amount you are billed each year for premiums generally stays pretty even.

Set forth below is a graph of the age of the insureds for the life settlements, as of June 30, 2022.

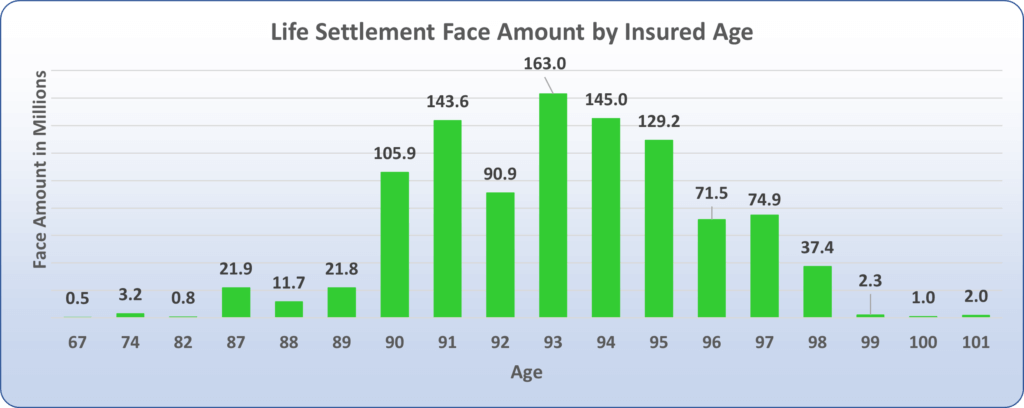

Set forth below is a graph of the face amount of the life settlements by the insured’s age. For example, we have $163.0 million in life settlement policies for insureds who are 93 years old, as of June 30, 2022.

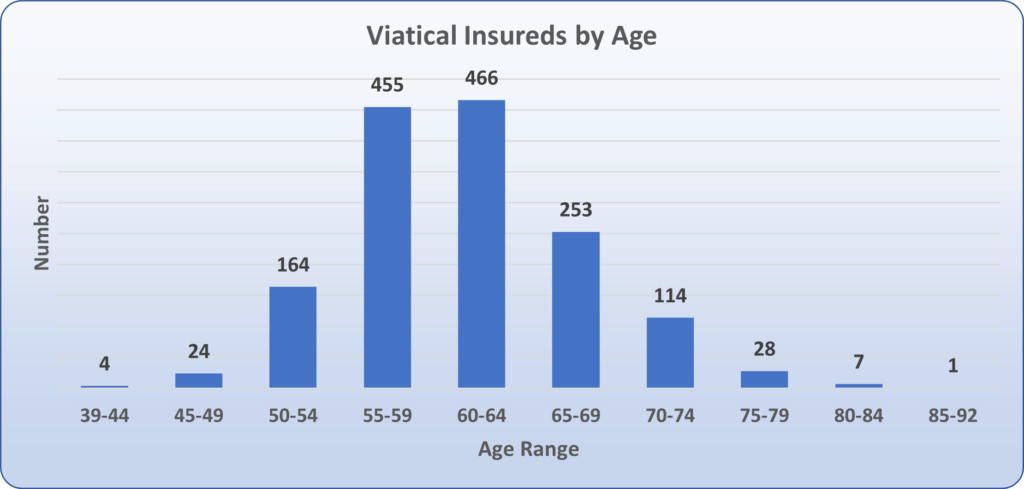

Set forth below is a graph of the age of the insureds for the viaticals, as of June 30, 2022.

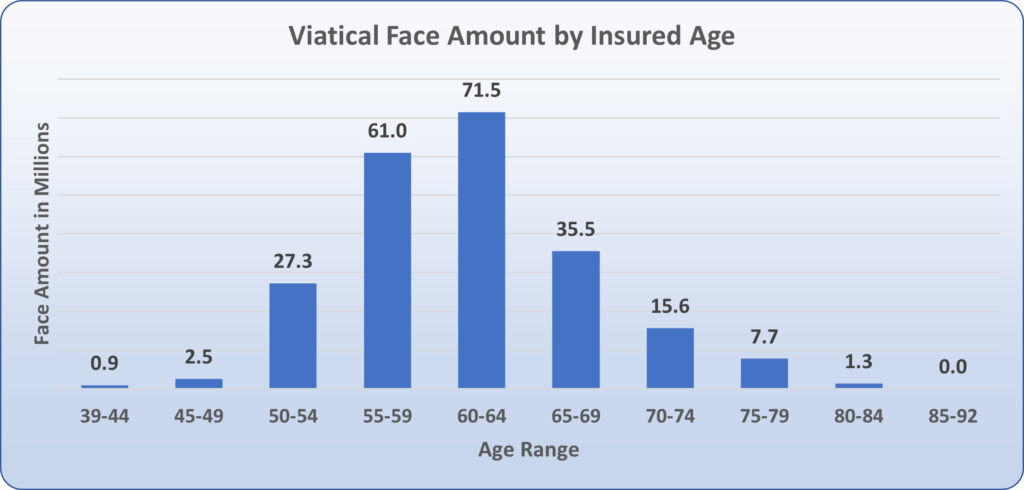

Set forth below is a graph of the face amount of the viaticals by the insured’s age. For example, we have $71.5 million in viaticals for insureds who are 60-64 years old, as of June 30, 2022.

How We Track Deaths of the Insureds

One of the most important functions of the Trust is to track the health, location and death of our insureds. Our servicer (NorthStar) attempts to contact each insured, either through phone calls or mailings, twice a year. We also monitor social media. We utilize different computer tracking services which search obituary and social security databases. In the industry, these are known as “crawlers” and they do these searches multiple times each week. In short, we are constantly trying to learn everything we can about whether an insured is alive or dead. These processes have been very successful and on average over the last year have learned of a death within 44 days after it occurs.

How We Get Paid and How You Get Paid

When the Trust learns that an insured has died, we immediately seek to obtain a death certificate from the state in which the insured died. Prior to the onset of COVID-19 the average time it took for the Trust to get a death certificate was 16 days. Once we receive the death certificate, we then complete the forms and paperwork required by that particular insurance company and submit a death claim. The insurance company then reviews the claim and if there are any questions or issues, we resolve them and then the insurance company issues and sends a check to ATLES. The average amount of time between submission of the death claim and receipt of the check by NorthStar is 19 days. Any delay in obtaining a death certificate or delay in paying the benefits by the insurance company in turn delays when ATLES receives the check. ATLES generally receives a check within 40 days after the death is discovered.

Once ATLES receives the funds, they are deposited into an ATLES bank account and those funds are paid to the Trust shortly after the end of the month. So, if a check is received in June the funds are paid to the Trust early in July. NorthStar then distributes those funds to each investor who holds an interest in the policy which paid the death benefits. That distribution usually occurs about the 15th of the month. So, funds received in one month are paid out by the 15th of the following month. If you owe a lien, it is deducted from what is paid to you. If you have unused funds in escrow those funds are also returned to you.

COVID-19 Impacts

While COVID-19 has not had any impact on the operations of the Trust, we have seen an impact on how long it takes to get paid after a death occurs. Prior to the onset of the virus it usually took the Trust about 16 days to obtain a death certificate for the person once we learned of the death. Since many government offices around the country closed their offices during the pandemic (in most instances a government office issues the death certificate) we saw a substantial slow-down in some states. The worst delays were in New York and unfortunately, we have a large concentration of insureds who reside in New York. We currently estimate the delay in obtaining a death certificate from New York to be six months. As government offices reopen, we remain hopeful that the delay is resolved.

Risks Associated with the Policies

There are a number of risks associated with both the life settlement and the viatical policies. Although we know where the vast majority of the life settlement insureds live, we have a small number of the insureds under the viaticals where we don’t know where they live (less than 1%). However, we do locate them once we learn of their death. These people are younger and many of them move around. Many of them travel or live in foreign countries. If they die in a foreign country, our ability to obtain a death certificate can become a challenge and it generally takes a long time to obtain one. In most instances we have to go through the US Embassy in that country and that is not an easy or fast process.

We have a substantial number of life settlement policies where the insurance coverage ends at age 100 which means the policy terminates, so if the insured has not died, we are out of luck. So far, we have not had any of those situations arise but as our insureds grow older, it could happen one day. As to the viaticals, a large number of them are term policies which means if the insured has not died by the end of the term, the policy terminates. In that Life Partners and subsequently the Trust have owned these policies for more than a couple of decades, we are starting to see some, but not many, of these policies terminate which means your investment in that policy would be lost. Other viatical policies have provisions in them that after a certain number of years the coverage reduces which means for example that a $50,000 policy could reduce to $35,000, or less. The value of your investment would reduce in turn. Some of the viatical policies are group life policies which is where a person works for a company and has insurance through a policy obtained by the company. If the person retires or is terminated or if the company goes out of business, coverage can terminate entirely.

It is also possible that an insurance company can refuse to pay the death benefits with respect to a life settlement if they think the policy is a “stranger-owned life insurance” policy which are illegal in some states. The Trust would vigorously contest those claims if made but it is still a risk.

Recent Maturities Where the Trust Has Been Paid

Updated as of 9-9-2022

Set forth below is a list of all policies where the death benefits have been received by the Trust with respect to a recent death AND those funds have not yet been disbursed to Continuing Fractional Holders (CFHs). As to these policies, your share of the death benefits will be mailed to you on or about the 15th day of the month following receipt by the Trust. So if the Trust receives a check in April your share will be distributed to you on or about the 15th of May.

Because the sale has closed, the Trustee will no longer update these lists. Please log-in to NorthStar’s Investor Portal for updates on your policies. The direct link to the Investor Portal is https://phtinvestor.northstarlife.com.

| Policy ID | Net Death Benefit | Date of Death | Discovered | Check Received | FundsDistributed |

|---|---|---|---|---|---|

| 9219 | 13,184.00 | 01/01/1970 | 11/07/2022 | 08/08/2022 | N |

| 10271 | 107,513.29 | 01/01/1970 | 01/01/1970 | 01/01/1970 | N |

| 10272 | 33,754.84 | 01/01/1970 | 01/01/1970 | 01/01/1970 | N |

| 22839 | 100,000.00 | 01/01/1970 | 01/01/1970 | 01/01/1970 | N |

| 22840 | 208,000.00 | 01/01/1970 | 01/01/1970 | 01/01/1970 | N |

| 29879 | 15,000.00 | 10/01/2022 | 01/01/1970 | 09/08/2022 | N |

| 31558 | 1,000,000.00 | 10/05/2022 | 01/01/1970 | 11/08/2022 | N |

| 39291 | 950,000.00 | 05/06/2022 | 01/01/1970 | 01/08/2022 | N |

| 72840 | 4,000,000.00 | 01/01/1970 | 01/01/1970 | 03/08/2022 | N |

Historical Maturities Where the Trust Has Been Paid

Set forth below is a list of all policies since inception of the Trust where the death benefits have been received by the Trust with respect to a death AND those funds have been disbursed to CFHs.

| Policy ID | Net Death Benefit | Date of Death | Discovered | Check Received | FundsDistributed |

|---|---|---|---|---|---|

| 3755 | 1,500,000.00 | 04/11/2019 | 11/11/2019 | 01/01/1970 | Y |

| 4733 | 80,000.00 | 08/03/2015 | 01/01/1970 | 01/01/1970 | Y |

| 4810 | 250,000.00 | 01/01/1970 | 01/01/1970 | 01/06/2018 | Y |

| 5537 | 50,000.00 | 11/09/2018 | 08/11/2019 | 01/01/1970 | Y |

| 5549 | 80,000.00 | 01/01/1970 | 11/03/2019 | 01/01/1970 | Y |

| 5901 | 2,000,000.00 | 01/01/1970 | 01/01/1970 | 01/07/2019 | Y |

| 6247 | 375,000.00 | 01/01/1970 | 01/01/1970 | 11/12/2017 | Y |

| 6248 | 625,000.00 | 01/01/1970 | 01/01/1970 | 11/12/2017 | Y |

| 6328 | 38,064.00 | 05/09/2021 | 01/01/1970 | 01/01/1970 | Y |

| 6556 | 2,000,000.00 | 12/08/2020 | 01/01/1970 | 01/01/1970 | Y |

| 6733 | 2,850,000.00 | 10/03/2017 | 01/01/1970 | 01/01/1970 | Y |

| 6883 | 10,000.00 | 01/01/1970 | 08/03/2021 | 01/01/1970 | Y |

| 7243 | 438,000.00 | 01/01/1970 | 01/01/1970 | 01/01/1970 | Y |

| 7245 | 25,000.00 | 01/01/1970 | 04/10/2021 | 01/03/2022 | Y |

| 7255 | 70,000.00 | 04/04/2021 | 12/04/2021 | 01/01/1970 | Y |

| 7256 | 50,000.00 | 04/04/2021 | 12/04/2021 | 01/01/1970 | Y |

| 7262 | 24,000.00 | 01/01/1970 | 01/01/1970 | 01/01/1970 | Y |

| 7263 | 50,000.00 | 01/01/1970 | 01/01/1970 | 01/01/1970 | Y |

| 7265 | 112,000.00 | 01/01/1970 | 01/01/1970 | 01/01/1970 | Y |

| 7289 | 150,000.00 | 01/01/1970 | 01/01/1970 | 01/01/1970 | Y |

| 7320 | 60,000.00 | 01/01/1970 | 05/02/2019 | 10/06/2019 | Y |

| 7356 | 30,000.00 | 08/05/2017 | 01/01/1970 | 12/06/2017 | Y |

| 7545 | 111,000.00 | 01/01/1970 | 01/01/1970 | 12/12/2019 | Y |

| 7546 | 17,076.92 | 01/01/1970 | 01/01/1970 | 12/12/2019 | Y |

| 7573 | 15,000.00 | 03/07/2019 | 01/01/1970 | 01/01/1970 | Y |

| 7591 | 115,113.00 | 01/01/1970 | 08/10/2019 | 01/01/1970 | Y |

| 7615 | 10,000.00 | 01/01/1970 | 04/06/2020 | 11/06/2020 | Y |

| 7617 | 15,000.00 | 01/01/1970 | 01/01/1970 | 05/03/2019 | Y |

| 7632 | 10,000.00 | 01/01/1970 | 01/01/1970 | 05/11/2021 | Y |

| 7633 | 20,000.00 | 01/01/1970 | 01/01/1970 | 08/11/2021 | Y |

| 7745 | 50,000.00 | 01/01/1970 | 01/01/1970 | 01/01/1970 | Y |

| 7786 | 141,000.00 | 01/01/1970 | 01/01/1970 | 01/01/1970 | Y |

| 7831 | 150,000.00 | 01/01/1970 | 01/01/1970 | 01/08/2018 | Y |

| 7857 | 100,000.00 | 01/01/1970 | 10/06/2020 | 07/07/2020 | Y |

| 7925 | 490,000.00 | 12/10/2021 | 01/01/1970 | 01/01/1970 | Y |

| 7926 | 99,000.00 | 12/10/2021 | 01/01/1970 | 01/01/1970 | Y |

| 7927 | 100,000.00 | 12/10/2021 | 01/01/1970 | 01/01/1970 | Y |

| 7928 | 500,000.00 | 12/10/2021 | 01/01/1970 | 01/01/1970 | Y |

| 7929 | 500,000.00 | 12/10/2021 | 01/01/1970 | 10/11/2021 | Y |

| 7950 | 134,760.43 | 01/01/1970 | 11/09/2019 | 01/01/1970 | Y |

| 7951 | 41,800.00 | 01/01/1970 | 11/09/2019 | 12/11/2019 | Y |

| 7961 | 25,000.00 | 03/02/2022 | 06/06/2022 | 11/07/2022 | Y |

| 8007 | 50,000.00 | 01/01/1970 | 10/02/2021 | 10/05/2021 | Y |

| 8012 | 51,867.62 | 01/01/1970 | 08/05/2017 | 01/01/1970 | Y |

| 8021 | 25,000.00 | 08/11/2017 | 01/01/1970 | 10/01/2018 | Y |

| 8192 | 40,766.45 | 01/01/1970 | 01/01/1970 | 01/01/1970 | Y |

| 8299 | 150,000.00 | 01/01/1970 | 01/01/1970 | 01/01/1970 | Y |

| 8442 | 31,630.00 | 09/11/2018 | 02/04/2019 | 01/01/1970 | Y |

| 8443 | 120,622.32 | 09/11/2018 | 02/04/2019 | 12/08/2019 | Y |

| 8558 | 80,000.00 | 01/01/1970 | 01/01/1970 | 01/01/1970 | Y |

| 8599 | 10,720.00 | 01/01/1970 | 04/01/2021 | 02/03/2021 | Y |

| 8600 | 6,000.00 | 01/01/1970 | 04/01/2021 | 02/03/2021 | Y |

| 8601 | 39,173.00 | 01/01/1970 | 04/01/2021 | 01/01/1970 | Y |

| 8603 | 16,884.00 | 01/01/1970 | 04/01/2021 | 08/03/2021 | Y |

| 8604 | 16,027.00 | 01/01/1970 | 04/01/2021 | 08/03/2021 | Y |

| 8611 | 22,566.28 | 10/02/2017 | 05/11/2018 | 01/01/1970 | Y |

| 8621 | 85,023.80 | 01/01/1970 | 01/01/1970 | 01/01/1970 | Y |

| 8623 | 80,000.00 | 01/01/1970 | 01/01/1970 | 12/10/2017 | Y |

| 8624 | 25,000.00 | 01/01/1970 | 01/01/1970 | 12/02/2018 | Y |

| 8625 | 100,000.00 | 01/01/1970 | 01/01/1970 | 09/10/2017 | Y |

| 8626 | 100,000.00 | 01/01/1970 | 01/01/1970 | 01/01/1970 | Y |

| 8628 | 85,000.00 | 01/01/1970 | 01/01/1970 | 01/01/1970 | Y |

| 8629 | 25,313.11 | 01/01/1970 | 01/01/1970 | 01/12/2017 | Y |

| 8644 | 66,000.00 | 01/01/1970 | 01/01/1970 | 02/01/2018 | Y |

| 8647 | 77,500.00 | 01/01/1970 | 01/01/1970 | 01/01/1970 | Y |

| 8682 | 50,000.00 | 09/04/2021 | 12/04/2021 | 11/05/2021 | Y |

| 8683 | 51,560.75 | 09/04/2021 | 12/04/2021 | 01/01/1970 | Y |

| 8686 | 10,000.00 | 09/04/2021 | 12/04/2021 | 01/01/1970 | Y |

| 8687 | 20,000.00 | 09/04/2021 | 12/04/2021 | 01/01/1970 | Y |

| 8699 | 65,234.00 | 01/01/1970 | 01/03/2022 | 04/04/2022 | Y |

| 8791 | 20,000.00 | 01/01/1970 | 01/01/1970 | 04/01/2022 | Y |

| 8848 | 115,000.00 | 08/12/2017 | 01/01/1970 | 01/01/1970 | Y |

| 8865 | 125,000.00 | 02/03/2018 | 07/03/2018 | 01/01/1970 | Y |

| 8909 | 19,452.00 | 01/01/1970 | 01/01/1970 | 11/03/2022 | Y |

| 8911 | 10,000.00 | 01/01/1970 | 01/01/1970 | 01/01/1970 | Y |

| 8933 | 648,000.00 | 01/01/1970 | 12/06/2020 | 01/01/1970 | Y |

| 8979 | 100,000.00 | 01/01/1970 | 01/01/1970 | 01/11/2021 | Y |

| 8993 | 100,000.00 | 01/01/1970 | 01/01/1970 | 01/01/1970 | Y |

| 8994 | 19,770.82 | 01/01/1970 | 01/01/1970 | 04/05/2017 | Y |

| 8997 | 25,000.00 | 01/01/1970 | 01/01/1970 | 04/04/2017 | Y |

| 9025 | 100,000.00 | 01/01/1970 | 07/01/2019 | 01/01/1970 | Y |

| 9090 | 55,365.78 | 01/01/1970 | 05/02/2019 | 08/03/2019 | Y |

| 9119 | 80,000.00 | 01/01/1970 | 05/06/2019 | 01/01/1970 | Y |

| 9199 | 25,000.00 | 02/05/2016 | 01/01/1970 | 01/01/1970 | Y |

| 9200 | 10,000.00 | 02/05/2016 | 01/01/1970 | 01/01/1970 | Y |

| 9201 | 50,000.00 | 02/05/2016 | 01/01/1970 | 01/01/1970 | Y |

| 9204 | 30,000.00 | 02/05/2016 | 01/01/1970 | 01/01/1970 | Y |

| 9305 | 51,432.59 | 01/01/1970 | 01/01/1970 | 04/12/2019 | Y |

| 9324 | 15,000.00 | 01/01/1970 | 01/01/1970 | 12/03/2018 | Y |

| 9351 | 31,064.00 | 01/01/1970 | 07/06/2019 | 01/01/1970 | Y |

| 9368 | 100,000.00 | 01/01/1970 | 01/01/1970 | 04/01/2018 | Y |

| 9381 | 145,000.00 | 01/01/1970 | 01/01/1970 | 02/12/2021 | Y |

| 9392 | 239,000.00 | 07/12/2017 | 01/01/1970 | 05/02/2018 | Y |

| 9409 | 10,000.00 | 01/01/1970 | 01/01/1970 | 01/01/1970 | Y |

| 9410 | 10,000.00 | 01/01/1970 | 01/01/1970 | 01/01/1970 | Y |

| 9411 | 11,790.00 | 01/01/1970 | 01/01/1970 | 01/01/1970 | Y |

| 9413 | 8,376.00 | 01/01/1970 | 01/01/1970 | 04/05/2020 | Y |

| 9415 | 10,000.00 | 01/01/1970 | 01/01/1970 | 01/01/1970 | Y |

| 9416 | 10,000.00 | 01/01/1970 | 01/01/1970 | 01/01/1970 | Y |

| 9417 | 12,500.00 | 01/01/1970 | 01/01/1970 | 01/01/1970 | Y |

| 9458 | 100,000.00 | 12/04/2006 | 08/07/2020 | 01/01/1970 | Y |

| 9471 | 141,160.73 | 12/07/2017 | 01/01/1970 | 01/01/1970 | Y |

| 9526 | 100,000.00 | 01/01/1970 | 05/03/2018 | 01/01/1970 | Y |

| 9543 | 84,000.00 | 01/01/1970 | 07/10/2019 | 04/11/2019 | Y |

| 9549 | 75,767.87 | 10/01/2021 | 01/01/1970 | 01/01/1970 | Y |

| 9684 | 20,000.00 | 01/01/1970 | 04/02/2020 | 02/03/2020 | Y |

| 9685 | 50,000.00 | 01/01/1970 | 04/02/2020 | 02/03/2020 | Y |

| 9757 | 41,605.08 | 01/01/1970 | 01/01/1970 | 07/09/2021 | Y |

| 9762 | 154,644.00 | 01/01/1970 | 04/03/2020 | 09/04/2020 | Y |

| 9764 | 40,000.00 | 01/01/1970 | 04/03/2020 | 01/01/1970 | Y |

| 9854 | 97,700.00 | 01/01/1970 | 01/01/1970 | 04/12/2018 | Y |

| 9855 | 91,075.23 | 01/01/1970 | 01/01/1970 | 01/01/1970 | Y |

| 9856 | 49,325.35 | 01/01/1970 | 01/01/1970 | 04/12/2018 | Y |

| 9905 | 90,000.00 | 01/01/1970 | 03/10/2018 | 01/01/1970 | Y |

| 9906 | 7,246.00 | 01/01/1970 | 03/10/2018 | 04/12/2018 | Y |

| 9921 | 40,000.00 | 03/06/2019 | 12/06/2019 | 01/01/1970 | Y |

| 9922 | 40,000.00 | 03/06/2019 | 12/06/2019 | 01/01/1970 | Y |

| 9996 | 98,295.07 | 01/01/1970 | 01/01/1970 | 01/01/1970 | Y |

| 10014 | 90,000.00 | 06/09/2020 | 01/01/1970 | 09/10/2020 | Y |

| 10015 | 50,000.00 | 06/09/2020 | 01/01/1970 | 12/10/2020 | Y |

| 10016 | 90,000.00 | 06/09/2020 | 01/01/1970 | 01/01/1970 | Y |

| 10017 | 10,000.00 | 06/09/2020 | 01/01/1970 | 01/01/1970 | Y |

| 10018 | 6,666.67 | 06/09/2020 | 01/01/1970 | 01/01/1970 | Y |

| 26925 | 3,333.33 | 06/09/2020 | 01/01/1970 | 01/01/1970 | Y |

| 10019 | 10,000.00 | 06/09/2020 | 01/01/1970 | 01/01/1970 | Y |

| 10020 | 6,000.00 | 06/09/2020 | 01/01/1970 | 01/01/1970 | Y |

| 26254 | 4,000.00 | 06/09/2020 | 01/01/1970 | 01/01/1970 | Y |

| 10058 | 25,000.00 | 01/01/1970 | 01/01/1970 | 01/01/1970 | Y |

| 10086 | 100,000.00 | 12/06/2018 | 01/01/1970 | 01/01/1970 | Y |

| 10087 | 96,185.00 | 12/06/2018 | 01/01/1970 | 01/01/1970 | Y |

| 10088 | 114,000.00 | 12/06/2018 | 01/01/1970 | 01/01/1970 | Y |

| 10205 | 50,000.00 | 01/01/1970 | 08/02/2021 | 01/01/1970 | Y |

| 10234 | 110,000.00 | 01/01/1970 | 01/01/1970 | 01/01/1970 | Y |

| 10283 | 103,264.00 | 04/12/2017 | 06/02/2018 | 01/01/1970 | Y |

| 10299 | 70,000.00 | 01/01/1970 | 01/01/1970 | 03/02/2020 | Y |

| 10300 | 40,000.00 | 01/01/1970 | 01/01/1970 | 01/01/1970 | Y |

| 10301 | 60,000.00 | 01/01/1970 | 01/01/1970 | 01/01/1970 | Y |

| 10311 | 60,000.00 | 01/01/1970 | 01/01/1970 | 01/01/1970 | Y |

| 10312 | 10,000.00 | 01/01/1970 | 01/01/1970 | 01/01/1970 | Y |

| 10342 | 25,000.00 | 01/01/1970 | 01/01/1970 | 03/08/2017 | Y |

| 10359 | 15,000.00 | 09/08/2018 | 01/01/1970 | 01/01/1970 | Y |

| 10360 | 9,000.00 | 09/08/2018 | 01/01/1970 | 01/01/1970 | Y |

| 10494 | 10,000.00 | 01/01/1970 | 10/12/2020 | 01/01/1970 | Y |

| 10495 | 20,000.00 | 01/01/1970 | 09/06/2022 | 11/07/2022 | Y |

| 10539 | 50,341.26 | 01/01/1970 | 01/01/1970 | 01/01/1970 | Y |

| 10557 | 30,814.83 | 02/05/2019 | 06/05/2019 | 01/01/1970 | Y |

| 10558 | 30,000.00 | 02/05/2019 | 06/05/2019 | 01/01/1970 | Y |

| 10609 | 98,562.00 | 01/01/1970 | 01/01/1970 | 01/01/1970 | Y |

| 10610 | 324,800.42 | 09/04/2020 | 01/01/1970 | 01/01/1970 | Y |

| 10611 | 49,393.60 | 09/04/2020 | 01/01/1970 | 01/01/1970 | Y |

| 10620 | 39,214.00 | 08/02/2021 | 09/03/2021 | 01/01/1970 | Y |

| 10655 | 37,464.22 | 01/01/1970 | 01/01/1970 | 02/05/2017 | Y |

| 10658 | 75,000.00 | 07/12/2017 | 01/01/1970 | 01/01/1970 | Y |

| 10709 | 99,676.00 | 01/01/1970 | 12/04/2021 | 08/06/2021 | Y |

| 10725 | 40,017.55 | 02/12/2018 | 01/10/2019 | 01/01/1970 | Y |

| 10760 | 70,500.00 | 01/01/1970 | 01/01/1970 | 01/01/1970 | Y |

| 10787 | 50,000.00 | 01/01/1970 | 01/01/1970 | 06/12/2017 | Y |

| 10794 | 62,000.00 | 01/01/1970 | 06/07/2017 | 07/09/2017 | Y |

| 10850 | 99,000.00 | 04/09/2020 | 02/10/2020 | 09/11/2020 | Y |

| 10858 | 79,000.00 | 01/01/1970 | 08/09/2021 | 05/01/2022 | Y |

| 10990 | 37,680.18 | 01/01/1970 | 01/01/1970 | 07/10/2019 | Y |

| 10992 | 100,000.00 | 01/01/1970 | 01/01/1970 | 01/01/1970 | Y |

| 11011 | 88,304.20 | 01/01/1970 | 01/01/1970 | 01/01/1970 | Y |

| 11107 | 30,000.00 | 01/01/1970 | 01/01/1970 | 01/01/1970 | Y |

| 11150 | 146,000.00 | 01/01/1970 | 01/01/1970 | 01/01/1970 | Y |

| 11151 | 200,000.00 | 01/01/1970 | 01/01/1970 | 01/01/1970 | Y |

| 11170 | 91,005.19 | 10/07/2020 | 01/01/1970 | 01/01/1970 | Y |

| 11171 | 30,335.06 | 10/07/2020 | 01/01/1970 | 01/01/1970 | Y |

| 11173 | 250,000.00 | 01/01/1970 | 01/01/1970 | 01/01/1970 | Y |

| 11196 | 47,875.86 | 07/11/2017 | 01/01/1970 | 01/01/1970 | Y |

| 11197 | 43,788.27 | 07/11/2017 | 01/01/1970 | 01/01/1970 | Y |

| 11198 | 42,654.38 | 07/11/2017 | 01/01/1970 | 01/01/1970 | Y |

| 11199 | 20,654.98 | 07/11/2017 | 01/01/1970 | 01/01/1970 | Y |

| 11202 | 132,000.00 | 07/11/2017 | 01/01/1970 | 01/01/1970 | Y |

| 11203 | 82,000.00 | 07/11/2017 | 01/01/1970 | 01/01/1970 | Y |

| 11243 | 30,000.00 | 08/04/2022 | 01/01/1970 | 10/06/2022 | Y |

| 11262 | 65,353.39 | 01/03/2022 | 10/03/2022 | 06/05/2022 | Y |

| 11263 | 25,000.00 | 01/03/2022 | 10/03/2022 | 01/01/1970 | Y |

| 11434 | 20,000.00 | 06/06/2020 | 01/01/1970 | 01/01/1970 | Y |

| 11474 | 100,000.00 | 01/01/1970 | 01/01/1970 | 01/01/1970 | Y |

| 11522 | 134,000.00 | 01/01/1970 | 12/10/2020 | 10/11/2020 | Y |

| 11593 | 20,000.00 | 09/02/2021 | 01/01/1970 | 01/01/1970 | Y |

| 11594 | 74,642.00 | 09/02/2021 | 01/01/1970 | 01/01/1970 | Y |

| 11595 | 10,000.00 | 09/02/2021 | 01/01/1970 | 06/04/2021 | Y |

| 11673 | 100,000.00 | 01/01/1970 | 10/06/2022 | 06/07/2022 | Y |

| 11832 | 80,000.00 | 09/11/2020 | 01/01/1970 | 01/01/1970 | Y |

| 11836 | 68,083.20 | 11/04/2017 | 01/05/2017 | 04/08/2017 | Y |

| 11837 | 42,552.00 | 11/04/2017 | 01/05/2017 | 01/01/1970 | Y |

| 11935 | 100,000.00 | 11/09/2018 | 08/11/2019 | 01/01/1970 | Y |

| 11940 | 40,000.00 | 11/09/2018 | 08/11/2019 | 09/12/2019 | Y |

| 11941 | 50,802.00 | 11/09/2018 | 08/11/2019 | 01/01/1970 | Y |

| 12132 | 15,084.88 | 01/01/1970 | 01/01/1970 | 01/01/1970 | Y |

| 12217 | 23,000.00 | 01/10/2020 | 01/01/1970 | 01/01/1970 | Y |

| 12384 | 15,000.00 | 01/01/1970 | 04/04/2018 | 01/01/1970 | Y |

| 12502 | 66,484.02 | 05/01/2018 | 09/01/2018 | 01/01/1970 | Y |

| 12536 | 102,164.10 | 01/01/1970 | 04/05/2020 | 01/01/1970 | Y |

| 12915 | 47,000.00 | 01/01/1970 | 06/08/2021 | 01/11/2021 | Y |

| 12925 | 40,416.00 | 01/01/1970 | 08/08/2019 | 12/09/2019 | Y |

| 13148 | 64,000.00 | 01/01/1970 | 01/01/1970 | 11/05/2021 | Y |

| 13223 | 120,477.72 | 01/01/1970 | 01/06/2022 | 01/01/1970 | Y |

| 13552 | 19,979.74 | 12/10/2017 | 01/01/1970 | 01/01/1970 | Y |

| 13553 | 6,120.00 | 12/10/2017 | 01/01/1970 | 06/11/2017 | Y |

| 13554 | 15,000.00 | 12/10/2017 | 01/01/1970 | 08/11/2017 | Y |

| 13949 | 37,025.64 | 04/03/2022 | 01/01/1970 | 05/07/2022 | Y |

| 13950 | 20,136.75 | 04/03/2022 | 01/01/1970 | 05/07/2022 | Y |

| 13951 | 18,837.61 | 04/03/2022 | 01/01/1970 | 05/07/2022 | Y |

| 13971 | 40,000.00 | 01/01/1970 | 01/01/1970 | 01/01/1970 | Y |

| 13979 | 10,000.00 | 01/03/2018 | 01/01/1970 | 10/04/2018 | Y |

| 14115 | 69,165.40 | 04/06/2021 | 01/01/1970 | 01/01/1970 | Y |

| 14117 | 70,000.00 | 04/06/2021 | 01/01/1970 | 07/09/2021 | Y |

| 14201 | 69,000.00 | 01/01/1970 | 01/01/1970 | 01/01/1970 | Y |

| 14252 | 55,000.00 | 03/12/2019 | 08/01/2020 | 05/02/2020 | Y |

| 14253 | 27,506.00 | 03/12/2019 | 08/01/2020 | 03/02/2020 | Y |

| 14656 | 10,000.00 | 01/01/1970 | 11/09/2020 | 01/01/1970 | Y |

| 14740 | 22,000.00 | 01/01/1970 | 01/01/1970 | 01/01/1970 | Y |

| 14823 | 98,534.02 | 01/01/1970 | 06/05/2022 | 01/06/2022 | Y |

| 6100 | 26,111.11 | 01/01/1970 | 01/01/1970 | 01/01/1970 | Y |

| 15160 | 73,888.89 | 01/01/1970 | 01/01/1970 | 01/01/1970 | Y |

| 15251 | 15,000.00 | 01/01/1970 | 01/01/1970 | 01/01/1970 | Y |

| 15397 | 200,000.00 | 01/01/1970 | 01/01/1970 | 01/01/1970 | Y |

| 15546 | 925,000.00 | 01/01/1970 | 12/02/2018 | 01/01/1970 | Y |

| 15552 | 57,000.00 | 01/01/1970 | 01/01/1970 | 01/01/1970 | Y |

| 15671 | 265,000.00 | 01/01/1970 | 01/01/1970 | 01/01/1970 | Y |

| 16011 | 206,000.00 | 01/01/1970 | 04/10/2021 | 01/01/1970 | Y |

| 16012 | 118,394.49 | 01/01/1970 | 04/10/2021 | 01/01/1970 | Y |

| 16022 | 20,000.00 | 01/01/1970 | 01/01/1970 | 01/01/1970 | Y |

| 16076 | 32,866.60 | 01/01/1970 | 01/01/1970 | 12/07/2021 | Y |

| 16079 | 66,906.69 | 01/01/1970 | 01/01/1970 | 12/07/2021 | Y |

| 16083 | 628,500.00 | 01/01/1970 | 01/01/1970 | 06/09/2017 | Y |

| 16526 | 70,500.00 | 01/01/1970 | 06/12/2016 | 01/01/1970 | Y |

| 16593 | 76,056.00 | 10/01/2022 | 01/01/1970 | 01/01/1970 | Y |

| 17042 | 65,000.00 | 02/12/2021 | 01/01/1970 | 01/01/1970 | Y |

| 17803 | 166,528.29 | 01/01/1970 | 02/05/2019 | 01/01/1970 | Y |

| 17882 | 75,821.84 | 01/01/1970 | 10/02/2020 | 01/01/1970 | Y |

| 17904 | 128,000.00 | 01/01/1970 | 01/01/1970 | 01/01/1970 | Y |

| 18130 | 250,000.00 | 01/01/1970 | 02/08/2019 | 01/01/1970 | Y |

| 18275 | 25,000.00 | 01/12/2020 | 07/12/2020 | 01/01/1970 | Y |

| 18296 | 118,219.69 | 01/01/1970 | 01/06/2021 | 01/01/1970 | Y |

| 18439 | 75,000.00 | 01/01/1970 | 01/01/1970 | 01/01/1970 | Y |

| 18441 | 10,000.00 | 06/04/2021 | 12/04/2021 | 10/05/2021 | Y |

| 18757 | 359,475.95 | 01/03/2018 | 07/03/2018 | 01/01/1970 | Y |

| 19201 | 100,000.00 | 01/01/1970 | 01/01/1970 | 01/01/1970 | Y |

| 19232 | 50,000.00 | 01/01/1970 | 01/01/1970 | 01/01/1970 | Y |

| 19420 | 359,000.00 | 10/07/2011 | 01/01/1970 | 06/12/2017 | Y |

| 19421 | 423,000.00 | 10/07/2011 | 01/01/1970 | 03/01/2018 | Y |

| 19461 | 100,000.00 | 01/01/1970 | 01/03/2017 | 11/12/2017 | Y |

| 19489 | 10,000.00 | 07/09/2015 | 05/06/2019 | 01/01/1970 | Y |

| 19536 | 25,018.00 | 06/02/2019 | 02/08/2019 | 01/01/1970 | Y |

| 19537 | 25,018.00 | 06/02/2019 | 02/08/2019 | 01/01/1970 | Y |

| 19838 | 205,085.46 | 12/02/2018 | 02/04/2018 | 01/01/1970 | Y |

| 20174 | 26,000.00 | 05/04/2022 | 01/01/1970 | 01/01/1970 | Y |

| 20759 | 35,000.00 | 01/01/1970 | 01/01/1970 | 07/05/2019 | Y |

| 20760 | 104,000.00 | 01/01/1970 | 01/01/1970 | 07/05/2019 | Y |

| 21308 | 15,000.00 | 01/01/1970 | 01/01/1970 | 08/11/2019 | Y |

| 21376 | 254,439.27 | 01/01/1970 | 07/08/2019 | 01/01/1970 | Y |

| 21635 | 166,618.43 | 01/01/1970 | 01/01/1970 | 01/01/1970 | Y |

| 21649 | 50,000.00 | 01/01/1970 | 01/01/1970 | 01/01/1970 | Y |

| 21650 | 200,000.00 | 01/01/1970 | 01/01/1970 | 01/01/1970 | Y |

| 21651 | 100,000.00 | 01/01/1970 | 01/01/1970 | 07/11/2019 | Y |

| 21692 | 50,000.00 | 04/10/2018 | 08/10/2018 | 06/11/2018 | Y |

| 21834 | 135,000.00 | 07/08/2017 | 08/09/2017 | 01/01/1970 | Y |

| 21932 | 92,253.53 | 03/08/2020 | 10/08/2020 | 08/09/2020 | Y |

| 21989 | 2,000,000.00 | 01/01/1970 | 01/01/1970 | 07/07/2020 | Y |

| 21991 | 2,000,000.00 | 01/01/1970 | 01/01/1970 | 09/07/2020 | Y |

| 21990 | 1,000,000.00 | 01/01/1970 | 01/01/1970 | 01/01/1970 | Y |

| 21992 | 1,000,000.00 | 01/01/1970 | 01/01/1970 | 01/01/1970 | Y |

| 22018 | 50,000.00 | 03/10/2019 | 01/01/1970 | 01/01/1970 | Y |

| 22021 | 75,000.00 | 03/10/2019 | 01/01/1970 | 01/01/1970 | Y |

| 22022 | 100,000.00 | 03/10/2019 | 01/01/1970 | 08/11/2019 | Y |

| 22024 | 98,300.00 | 03/10/2019 | 01/01/1970 | 01/01/1970 | Y |

| 22143 | 95,000.00 | 01/01/1970 | 01/01/1970 | 11/07/2017 | Y |

| 22163 | 200,000.00 | 01/01/1970 | 06/06/2018 | 01/01/1970 | Y |

| 22203 | 32,000.00 | 01/01/1970 | 01/01/1970 | 01/01/1970 | Y |

| 22204 | 118,688.00 | 01/01/1970 | 01/01/1970 | 05/05/2022 | Y |

| 22207 | 300,000.00 | 01/01/1970 | 01/01/1970 | 01/01/1970 | Y |

| 22208 | 564,000.00 | 01/01/1970 | 01/01/1970 | 01/01/1970 | Y |

| 22214 | 564,000.00 | 01/01/1970 | 01/01/1970 | 01/01/1970 | Y |

| 22213 | 100,000.00 | 01/01/1970 | 01/01/1970 | 10/05/2022 | Y |

| 22357 | 15,000.00 | 04/05/2017 | 01/01/1970 | 06/09/2017 | Y |

| 22371 | 100,000.00 | 01/01/1970 | 01/01/1970 | 01/01/1970 | Y |

| 22392 | 35,726.60 | 01/01/1970 | 01/01/1970 | 10/02/2022 | Y |

| 22409 | 245,760.00 | 01/01/1970 | 05/12/2016 | 09/02/2017 | Y |

| 22427 | 250,493.45 | 01/01/1970 | 11/06/2020 | 03/08/2020 | Y |

| 22444 | 168,000.00 | 11/02/2019 | 06/03/2019 | 08/04/2019 | Y |

| 22450 | 60,000.00 | 07/04/2017 | 08/06/2017 | 01/01/1970 | Y |

| 22477 | 50,000.00 | 07/09/2017 | 01/01/1970 | 03/11/2017 | Y |

| 22572 | 125,000.00 | 01/01/1970 | 01/01/1970 | 01/01/1970 | Y |

| 22575 | 50,000.00 | 03/04/2020 | 01/01/1970 | 01/01/1970 | Y |

| 22584 | 26,376.66 | 11/06/2020 | 01/01/1970 | 01/01/1970 | Y |

| 22585 | 40,000.00 | 11/06/2020 | 01/01/1970 | 01/01/1970 | Y |

| 22596 | 100,000.00 | 01/01/1970 | 01/01/1970 | 08/05/2020 | Y |

| 22742 | 100,000.00 | 01/01/1970 | 10/06/2020 | 01/01/1970 | Y |

| 22795 | 50,000.00 | 02/01/2019 | 01/01/1970 | 04/02/2019 | Y |

| 22968 | 39,753.00 | 01/01/1970 | 01/01/1970 | 01/01/1970 | Y |

| 23001 | 97,711.00 | 01/01/1970 | 01/04/2019 | 07/10/2019 | Y |

| 23080 | 70,000.00 | 05/10/2014 | 01/01/1970 | 09/08/2019 | Y |

| 23106 | 50,790.00 | 06/04/2020 | 01/01/1970 | 01/01/1970 | Y |

| 23143 | 20,000.00 | 01/01/1970 | 01/01/1970 | 04/11/2020 | Y |

| 23145 | 292,000.00 | 01/01/1970 | 01/01/1970 | 04/11/2020 | Y |

| 23150 | 792,000.00 | 04/03/2017 | 09/03/2017 | 01/01/1970 | Y |

| 23166 | 10,000.00 | 01/01/1970 | 01/10/2018 | 05/10/2018 | Y |

| 23173 | 38,000.00 | 06/09/2018 | 01/01/1970 | 01/01/1970 | Y |

| 23258 | 105,770.73 | 12/10/2016 | 08/05/2018 | 08/06/2018 | Y |

| 23281 | 178,599.94 | 01/01/1970 | 04/02/2019 | 01/01/1970 | Y |

| 23374 | 250,000.00 | 01/01/1970 | 04/09/2018 | 01/01/1970 | Y |

| 23483 | 25,000.00 | 01/01/1970 | 04/01/2022 | 01/01/1970 | Y |

| 23647 | 270,000.00 | 01/01/1970 | 01/01/1970 | 01/01/1970 | Y |

| 23756 | 200,000.00 | 01/01/1970 | 01/01/1970 | 04/05/2017 | Y |

| 23954 | 51,400.00 | 01/01/1970 | 05/01/2017 | 08/12/2017 | Y |

| 24037 | 58,392.52 | 01/01/1970 | 01/01/1970 | 01/01/1970 | Y |

| 24038 | 29,607.48 | 01/01/1970 | 01/01/1970 | 01/01/1970 | Y |

| 24395 | 29,000.00 | 12/04/2019 | 01/01/1970 | 01/01/1970 | Y |

| 24564 | 50,000.00 | 09/01/2019 | 01/01/1970 | 01/01/1970 | Y |

| 24705 | 82,150.00 | 01/01/1970 | 01/01/1970 | 11/07/2018 | Y |

| 24806 | 1,500,000.00 | 01/01/1970 | 01/01/1970 | 01/01/1970 | Y |

| 24807 | 595,059.00 | 01/01/1970 | 01/01/1970 | 01/01/1970 | Y |

| 25115 | 72,000.00 | 01/01/1970 | 10/01/2017 | 10/04/2017 | Y |

| 25143 | 600,000.00 | 01/01/1970 | 01/01/1970 | 01/01/1970 | Y |

| 25290 | 400,000.00 | 01/01/1970 | 01/01/1970 | 01/01/1970 | Y |

| 25306 | 82,316.03 | 01/01/1970 | 01/01/1970 | 10/08/2021 | Y |

| 25345 | 1,250,000.00 | 06/11/2016 | 01/01/1970 | 10/02/2017 | Y |

| 25369 | 1,000,000.00 | 05/05/2020 | 11/05/2020 | 05/06/2020 | Y |

| 25370 | 3,000,000.00 | 05/05/2020 | 11/05/2020 | 09/07/2020 | Y |

| 25379 | 1,000,000.00 | 03/10/2017 | 12/10/2017 | 08/11/2017 | Y |

| 25387 | 350,000.00 | 10/04/2022 | 01/01/1970 | 11/05/2022 | Y |

| 25415 | 96,828.80 | 09/12/2017 | 01/01/1970 | 01/01/1970 | Y |

| 25417 | 400,000.00 | 01/01/1970 | 01/01/1970 | 03/04/2019 | Y |

| 25430 | 228,000.00 | 12/11/2017 | 04/12/2017 | 01/01/1970 | Y |

| 25431 | 10,000.00 | 01/01/1970 | 02/06/2021 | 01/01/1970 | Y |

| 25442 | 100,000.00 | 01/01/1970 | 01/08/2019 | 03/09/2019 | Y |

| 25448 | 500,000.00 | 01/01/1970 | 12/06/2020 | 08/07/2020 | Y |

| 25461 | 700,000.00 | 05/05/2020 | 01/01/1970 | 01/01/1970 | Y |

| 25503 | 540,000.00 | 05/01/2020 | 01/01/1970 | 04/03/2020 | Y |

| 25510 | 29,057.11 | 01/01/1970 | 05/08/2019 | 01/01/1970 | Y |

| 25535 | 150,000.00 | 05/12/2019 | 01/01/1970 | 01/01/1970 | Y |

| 25708 | 75,000.00 | 01/01/1970 | 08/01/2020 | 03/02/2020 | Y |

| 25869 | 95,000.00 | 10/05/2018 | 01/01/1970 | 06/08/2018 | Y |

| 26004 | 1,000,000.00 | 01/01/1970 | 10/02/2021 | 01/01/1970 | Y |

| 26278 | 58,506.15 | 12/07/2021 | 01/01/1970 | 01/01/1970 | Y |

| 26286 | 50,000.00 | 03/12/2018 | 12/12/2018 | 01/01/1970 | Y |

| 26426 | 1,300,000.00 | 01/01/1970 | 01/01/1970 | 02/08/2017 | Y |

| 26667 | 1,000,000.00 | 01/01/1970 | 05/10/2017 | 01/01/1970 | Y |

| 26889 | 75,000.00 | 01/01/1970 | 08/01/2020 | 03/02/2020 | Y |

| 27164 | 2,000,000.00 | 01/01/1970 | 01/01/1970 | 03/05/2018 | Y |

| 27235 | 2,000,000.00 | 01/01/1970 | 01/01/1970 | 01/01/1970 | Y |

| 27350 | 2,022,167.44 | 03/05/2019 | 01/01/1970 | 01/01/1970 | Y |

| 27509 | 250,000.00 | 02/12/2017 | 11/12/2017 | 01/01/1970 | Y |

| 27778 | 42,000.00 | 07/07/2020 | 01/01/1970 | 01/01/1970 | Y |

| 28078 | 50,000.00 | 01/01/1970 | 08/01/2020 | 01/01/1970 | Y |

| 28109 | 100,000.00 | 03/12/2018 | 12/12/2018 | 01/01/1970 | Y |

| 28559 | 500,000.00 | 01/01/1970 | 01/01/1970 | 05/10/2017 | Y |

| 28947 | 100,000.00 | 01/01/1970 | 01/01/1970 | 01/01/1970 | Y |

| 29218 | 62,000.00 | 07/11/2017 | 01/01/1970 | 01/12/2017 | Y |

| 39346 | 60,000.00 | 07/11/2017 | 01/01/1970 | 01/12/2017 | Y |

| 29603 | 150,000.00 | 09/10/2021 | 06/06/2022 | 01/01/1970 | Y |

| 29860 | 175,000.00 | 08/04/2020 | 01/01/1970 | 01/01/1970 | Y |

| 29944 | 400,000.00 | 01/01/1970 | 06/07/2020 | 02/09/2020 | Y |

| 30091 | 50,000.00 | 11/07/2017 | 12/09/2018 | 05/10/2018 | Y |

| 30222 | 375,000.00 | 01/01/1970 | 01/01/1970 | 10/08/2020 | Y |

| 30340 | 804,052.00 | 04/02/2017 | 01/01/1970 | 01/01/1970 | Y |

| 30541 | 684,931.00 | 01/01/1970 | 04/06/2018 | 02/07/2018 | Y |

| 30817 | 1,920,813.00 | 01/09/2017 | 05/09/2017 | 01/01/1970 | Y |

| 30901 | 350,000.00 | 01/01/1970 | 01/01/1970 | 01/01/1970 | Y |

| 31203 | 200,000.00 | 01/01/1970 | 01/01/1970 | 02/06/2017 | Y |

| 31837 | 500,000.00 | 01/01/1970 | 01/03/2021 | 08/04/2021 | Y |

| 31949 | 1,000,000.00 | 01/01/1970 | 01/01/1970 | 01/01/1970 | Y |

| 31962 | 1,700,000.00 | 01/01/1970 | 01/01/1970 | 01/01/1970 | Y |

| 32043 | 54,416.28 | 10/08/2019 | 01/01/1970 | 03/09/2019 | Y |

| 32051 | 2,000,000.00 | 08/05/2017 | 11/05/2017 | 01/01/1970 | Y |

| 32117 | 1,000,000.00 | 08/09/2019 | 01/01/1970 | 09/10/2019 | Y |

| 32118 | 1,000,000.00 | 08/09/2019 | 01/01/1970 | 10/10/2019 | Y |

| 32139 | 92,280.00 | 01/01/1970 | 12/10/2021 | 01/01/1970 | Y |

| 32140 | 57,240.00 | 01/01/1970 | 12/10/2021 | 01/01/1970 | Y |

| 32141 | 53,160.00 | 01/01/1970 | 12/10/2021 | 01/01/1970 | Y |

| 32142 | 22,500.00 | 01/01/1970 | 12/10/2021 | 01/01/1970 | Y |

| 32143 | 32,500.00 | 01/01/1970 | 12/10/2021 | 01/01/1970 | Y |

| 32144 | 40,000.00 | 01/01/1970 | 12/10/2021 | 01/01/1970 | Y |

| 32145 | 36,000.00 | 01/01/1970 | 12/10/2021 | 01/01/1970 | Y |

| 32147 | 50,000.00 | 01/01/1970 | 01/01/1970 | 06/04/2018 | Y |

| 32600 | 100,000.00 | 06/01/2018 | 08/01/2018 | 10/05/2018 | Y |

| 32601 | 150,000.00 | 06/01/2018 | 08/01/2018 | 10/05/2018 | Y |

| 32692 | 657,125.00 | 01/01/1970 | 01/01/1970 | 01/01/1970 | Y |

| 32978 | 37,500.00 | 07/07/2020 | 01/01/1970 | 01/01/1970 | Y |

| 33025 | 175,000.00 | 07/07/2020 | 01/01/1970 | 01/01/1970 | Y |

| 33034 | 3,750,000.00 | 12/01/2021 | 01/01/1970 | 01/01/1970 | Y |

| 33084 | 10,000.00 | 01/01/1970 | 01/01/1970 | 01/01/1970 | Y |

| 33289 | 10,000,000.00 | 01/11/2021 | 12/11/2021 | 01/01/1970 | Y |

| 33408 | 2,000,000.00 | 01/01/1970 | 01/01/1970 | 06/10/2017 | Y |

| 33462 | 500,000.00 | 01/01/1970 | 01/01/1970 | 01/01/1970 | Y |

| 33464 | 500,000.00 | 01/01/1970 | 01/01/1970 | 01/01/1970 | Y |

| 33897 | 500,000.00 | 10/04/2020 | 01/01/1970 | 01/01/1970 | Y |

| 34477 | 10,000.21 | 05/11/2019 | 01/01/1970 | 08/09/2020 | Y |

| 35681 | 500,000.00 | 04/08/2018 | 01/01/1970 | 01/01/1970 | Y |

| 36449 | 2,500,000.00 | 10/03/2019 | 07/05/2019 | 01/01/1970 | Y |

| 36987 | 9,300,000.00 | 01/01/1970 | 01/01/1970 | 01/01/1970 | Y |

| 37758 | 5,000,000.00 | 04/09/2021 | 01/01/1970 | 01/01/1970 | Y |

| 39281 | 400,000.00 | 01/01/1970 | 01/01/1970 | 08/05/2019 | Y |

| 39607 | 2,500,000.00 | 08/03/2022 | 01/01/1970 | 01/01/1970 | Y |

| 39656 | 5,000,000.00 | 07/01/2019 | 01/01/1970 | 05/04/2019 | Y |

| 39857 | 2,848,617.00 | 05/10/2018 | 01/01/1970 | 09/11/2018 | Y |

| 40090 | 225,000.00 | 01/01/1970 | 01/01/1970 | 01/01/1970 | Y |

| 40255 | 52,500.00 | 01/01/1970 | 03/12/2020 | 01/01/1970 | Y |

| 40290 | 500,000.00 | 01/01/1970 | 02/05/2022 | 01/01/1970 | Y |

| 40307 | 2,000,000.00 | 01/01/1970 | 01/01/1970 | 01/01/1970 | Y |

| 40354 | 15,000.00 | 01/01/1970 | 01/01/1970 | 06/07/2020 | Y |

| 40355 | 25,000.00 | 01/01/1970 | 01/01/1970 | 01/01/1970 | Y |

| 40535 | 500,000.00 | 01/01/1970 | 01/01/1970 | 01/01/1970 | Y |

| 40842 | 10,000,000.00 | 11/03/2021 | 12/03/2021 | 01/01/1970 | Y |

| 40973 | 100,000.00 | 01/01/1970 | 02/03/2020 | 01/01/1970 | Y |

| 41195 | 62,000.00 | 07/11/2017 | 01/01/1970 | 01/01/1970 | Y |

| 41280 | 100,469.63 | 01/01/1970 | 02/08/2019 | 01/01/1970 | Y |

| 41639 | 600,000.00 | 02/10/2020 | 01/01/1970 | 04/01/2021 | Y |

| 41640 | 1,000,000.00 | 02/10/2020 | 01/01/1970 | 12/01/2021 | Y |

| 41766 | 5,000,000.00 | 01/01/1970 | 07/04/2020 | 01/01/1970 | Y |

| 42303 | 5,000,000.00 | 07/01/2019 | 01/01/1970 | 05/04/2019 | Y |

| 42304 | 5,000,000.00 | 07/01/2019 | 01/01/1970 | 05/04/2019 | Y |

| 42362 | 1,250,000.00 | 01/01/1970 | 01/01/1970 | 05/03/2018 | Y |

| 42396 | 1,000,000.00 | 01/01/1970 | 01/01/1970 | 10/07/2020 | Y |

| 42523 | 700,000.00 | 01/01/1970 | 01/01/1970 | 01/01/1970 | Y |

| 43457 | 5,000,000.00 | 01/07/2018 | 10/07/2018 | 01/01/1970 | Y |

| 43460 | 5,000,000.00 | 01/07/2018 | 10/07/2018 | 01/01/1970 | Y |

| 43471 | 100,000.00 | 01/01/1970 | 01/01/1970 | 01/01/1970 | Y |

| 43517 | 2,500,000.00 | 02/04/2020 | 03/04/2020 | 01/01/1970 | Y |

| 43523 | 5,000,000.00 | 01/01/1970 | 01/01/1970 | 04/01/2022 | Y |

| 43578 | 5,000,000.00 | 01/01/1970 | 01/01/1970 | 01/01/1970 | Y |

| 44254 | 5,000,000.00 | 04/07/2019 | 01/01/1970 | 01/01/1970 | Y |

| 44501 | 5,000,000.00 | 01/01/1970 | 01/05/2019 | 01/01/1970 | Y |

| 44580 | 500,000.00 | 01/01/1970 | 01/01/1970 | 01/01/1970 | Y |

| 44599 | 500,000.00 | 04/07/2019 | 10/07/2019 | 01/01/1970 | Y |

| 44633 | 1,000,000.00 | 09/05/2021 | 01/01/1970 | 08/06/2021 | Y |

| 44641 | 1,000,000.00 | 01/01/1970 | 01/01/1970 | 02/11/2021 | Y |

| 44692 | 1,000,000.00 | 08/05/2022 | 01/01/1970 | 01/01/1970 | Y |

| 44737 | 10,000,000.00 | 06/05/2022 | 01/01/1970 | 01/01/1970 | Y |

| 45538 | 5,000,000.00 | 01/01/1970 | 09/12/2019 | 01/01/1970 | Y |

| 45719 | 2,000,000.00 | 09/03/2019 | 01/01/1970 | 12/06/2019 | Y |

| 46597 | 10,000,000.00 | 10/11/2018 | 01/01/1970 | 07/12/2018 | Y |

| 46606 | 1,000,000.00 | 01/01/1970 | 01/01/1970 | 01/01/1970 | Y |

| 46734 | 1,000,000.00 | 01/01/1970 | 01/01/1970 | 01/01/1970 | Y |

| 46796 | 350,000.00 | 01/01/1970 | 01/01/1970 | 09/10/2018 | Y |

| 47499 | 5,000,000.00 | 07/08/2020 | 12/08/2020 | 01/01/1970 | Y |

| 47580 | 1,000,000.00 | 01/01/1970 | 01/01/1970 | 11/03/2022 | Y |

| 48846 | 11,500,000.00 | 01/01/1970 | 01/01/1970 | 03/08/2017 | Y |

| 48962 | 500,000.00 | 01/01/1970 | 01/01/1970 | 01/01/1970 | Y |

| 49559 | 4,000,000.00 | 01/04/2017 | 01/01/1970 | 01/01/1970 | Y |

| 50107 | 7,500,000.00 | 01/01/1970 | 01/01/1970 | 01/01/1970 | Y |

| 50224 | 10,000,000.00 | 08/01/2022 | 01/01/1970 | 09/02/2022 | Y |

| 51528 | 5,000,000.00 | 01/01/1970 | 01/01/1970 | 01/01/1970 | Y |

| 52618 | 8,250,000.00 | 01/01/1970 | 01/01/1970 | 08/07/2020 | Y |

| 52920 | 30,000.00 | 11/09/2018 | 08/11/2019 | 01/01/1970 | Y |

| 53878 | 5,000,000.00 | 01/01/1970 | 01/01/1970 | 01/01/1970 | Y |

| 53935 | 1,000,000.00 | 01/01/1970 | 01/01/1970 | 01/01/1970 | Y |

| 54320 | 3,000,000.00 | 01/01/1970 | 05/04/2021 | 02/06/2021 | Y |

| 54445 | 1,315,000.00 | 01/01/1970 | 12/09/2017 | 02/10/2017 | Y |

| 54525 | 15,000,000.00 | 02/01/2020 | 06/01/2020 | 05/02/2020 | Y |

| 54571 | 6,000,000.00 | 10/02/2017 | 01/01/1970 | 04/04/2017 | Y |

| 54667 | 5,000,000.00 | 01/01/1970 | 01/01/1970 | 01/01/1970 | Y |

| 55078 | 1,000,000.00 | 01/01/1970 | 01/01/1970 | 01/11/2019 | Y |

| 55103 | 350,000.00 | 01/01/1970 | 01/01/1970 | 01/01/1970 | Y |

| 55107 | 350,000.00 | 01/01/1970 | 01/01/1970 | 01/01/1970 | Y |

| 55781 | 5,000,000.00 | 01/01/1970 | 01/04/2020 | 01/01/1970 | Y |

| 56035 | 5,000,000.00 | 10/08/2019 | 12/08/2019 | 01/01/1970 | Y |

| 56041 | 5,000,000.00 | 10/08/2019 | 12/08/2019 | 01/01/1970 | Y |

| 56042 | 5,000,000.00 | 10/08/2019 | 12/08/2019 | 01/01/1970 | Y |

| 56404 | 2,000,000.00 | 01/01/1970 | 01/04/2020 | 11/05/2020 | Y |

| 56604 | 2,000,000.00 | 01/01/1970 | 07/05/2018 | 01/01/1970 | Y |

| 57139 | 252,680.27 | 01/01/1970 | 01/01/1970 | 01/01/1970 | Y |

| 58816 | 1,000,000.00 | 01/01/1970 | 03/06/2019 | 01/01/1970 | Y |

| 59327 | 6,000,000.00 | 01/01/1970 | 02/08/2021 | 01/01/1970 | Y |

| 59898 | 2,500,000.00 | 05/03/2021 | 11/03/2021 | 01/06/2021 | Y |

| 59937 | 1,000,000.00 | 11/06/2018 | 12/06/2018 | 03/07/2018 | Y |

| 60099 | 500,000.00 | 03/03/2019 | 01/04/2019 | 01/01/1970 | Y |

| 60249 | 4,000,000.00 | 01/02/2018 | 01/01/1970 | 07/03/2018 | Y |

| 60772 | 1,000,000.00 | 01/01/1970 | 09/04/2020 | 06/05/2020 | Y |

| 60914 | 400,000.00 | 05/11/2020 | 09/11/2020 | 04/01/2021 | Y |

| 60993 | 500,000.00 | 01/01/1970 | 01/01/1970 | 01/01/1970 | Y |

| 61187 | 5,000,000.00 | 03/08/2019 | 06/08/2019 | 01/01/1970 | Y |

| 61188 | 5,000,000.00 | 03/08/2019 | 06/08/2019 | 01/01/1970 | Y |

| 61278 | 4,000,000.00 | 10/09/2019 | 01/01/1970 | 01/01/1970 | Y |

| 61281 | 2,876,787.00 | 10/09/2019 | 01/01/1970 | 02/10/2019 | Y |

| 61730 | 5,000,000.00 | 01/01/1970 | 01/01/1970 | 01/01/1970 | Y |

| 61923 | 5,000,000.00 | 01/03/2018 | 07/03/2018 | 05/04/2018 | Y |

| 62439 | 10,000,000.00 | 01/01/1970 | 03/12/2018 | 01/01/1970 | Y |

| 62454 | 5,000,000.00 | 03/08/2018 | 06/08/2018 | 01/01/1970 | Y |

| 62507 | 200,000.00 | 01/01/1970 | 03/08/2017 | 01/01/1970 | Y |

| 62689 | 5,000,000.00 | 01/01/1970 | 04/09/2018 | 04/10/2018 | Y |

| 63648 | 1,000,000.00 | 01/01/2022 | 11/01/2022 | 01/01/1970 | Y |

| 63660 | 5,000,000.00 | 03/10/2020 | 01/01/1970 | 08/01/2021 | Y |

| 64647 | 400,000.00 | 11/09/2019 | 01/01/1970 | 03/02/2020 | Y |

| 64700 | 2,000,000.00 | 01/01/1970 | 01/01/1970 | 01/01/1970 | Y |

| 64706 | 5,000,000.00 | 02/05/2021 | 10/05/2021 | 01/01/1970 | Y |

| 64877 | 1,000,000.00 | 01/01/1970 | 01/01/1970 | 12/06/2019 | Y |

| 64997 | 250,000.00 | 01/01/1970 | 01/01/1970 | 05/10/2020 | Y |

| 65570 | 350,000.00 | 05/12/2020 | 08/12/2020 | 12/01/2021 | Y |

| 65571 | 4,500,000.00 | 01/04/2020 | 01/01/1970 | 07/05/2020 | Y |

| 65714 | 1,000,000.00 | 01/01/1970 | 01/01/1970 | 12/10/2018 | Y |

| 65866 | 2,000,000.00 | 01/05/2018 | 01/01/1970 | 07/06/2018 | Y |

| 66118 | 10,000,000.00 | 09/01/2017 | 01/01/1970 | 01/01/1970 | Y |

| 66373 | 3,000,000.00 | 01/01/1970 | 01/01/1970 | 01/12/2017 | Y |

| 66655 | 3,000,000.00 | 01/01/1970 | 01/01/1970 | 01/01/1970 | Y |

| 66894 | 2,000,000.00 | 10/08/2021 | 01/09/2021 | 01/01/1970 | Y |

| 67184 | 500,000.00 | 03/12/2019 | 03/12/2019 | 06/01/2020 | Y |

| 67251 | 1,000,000.00 | 11/01/2021 | 01/01/1970 | 01/01/1970 | Y |

| 67330 | 255,507.01 | 01/01/1970 | 01/01/1970 | 08/10/2021 | Y |

| 67331 | 510,749.12 | 01/01/1970 | 01/01/1970 | 08/10/2021 | Y |

| 67332 | 255,690.74 | 01/01/1970 | 01/01/1970 | 08/10/2021 | Y |

| 67342 | 511,363.69 | 01/01/1970 | 01/01/1970 | 08/10/2021 | Y |

| 67612 | 2,500,000.00 | 01/01/1970 | 01/01/1970 | 01/01/1970 | Y |

| 67848 | 4,000,000.00 | 01/01/1970 | 07/04/2022 | 01/01/1970 | Y |

| 68054 | 5,000,000.00 | 01/01/1970 | 09/07/2019 | 01/01/1970 | Y |

| 68406 | 1,500,000.00 | 01/01/1970 | 07/07/2021 | 01/01/1970 | Y |

| 68461 | 4,000,000.00 | 01/01/1970 | 12/04/2021 | 01/01/1970 | Y |

| 68674 | 1,500,000.00 | 01/01/1970 | 02/03/2021 | 01/01/1970 | Y |

| 68766 | 4,500,000.00 | 02/01/2021 | 07/04/2022 | 03/05/2022 | Y |

| 68801 | 5,000,000.00 | 01/01/1970 | 09/07/2019 | 01/01/1970 | Y |

| 69296 | 2,000,000.00 | 01/01/1970 | 01/01/1970 | 12/10/2017 | Y |

| 69779 | 1,500,000.00 | 01/01/1970 | 01/01/1970 | 11/03/2022 | Y |

| 69954 | 2,000,000.00 | 06/04/2020 | 07/04/2020 | 01/01/1970 | Y |

| 70002 | 1,150,000.00 | 01/01/1970 | 01/01/1970 | 06/08/2020 | Y |

| 70070 | 399,975.00 | 01/01/1970 | 01/01/1970 | 01/01/1970 | Y |

| 70097 | 4,000,000.00 | 03/11/2020 | 09/11/2020 | 01/01/1970 | Y |

| 70170 | 1,000,000.00 | 10/11/2019 | 01/01/1970 | 04/12/2019 | Y |

| 70357 | 2,000,000.00 | 01/01/1970 | 01/01/1970 | 01/01/1970 | Y |

| 70358 | 250,000.00 | 04/03/2017 | 01/01/1970 | 07/04/2017 | Y |

| 70373 | 5,000,000.00 | 01/01/1970 | 01/01/1970 | 01/01/1970 | Y |

| 70407 | 4,000,000.00 | 02/01/2021 | 07/04/2022 | 06/05/2022 | Y |

| 70497 | 7,000,000.00 | 10/10/2018 | 12/10/2018 | 11/12/2018 | Y |

| 70517 | 700,000.00 | 07/07/2017 | 01/01/1970 | 01/01/1970 | Y |

| 70548 | 4,500,000.00 | 04/02/2021 | 01/01/1970 | 03/06/2021 | Y |

| 71157 | 500,000.00 | 08/07/2017 | 01/01/1970 | 01/01/1970 | Y |

| 71186 | 5,000,000.00 | 01/01/1970 | 01/01/1970 | 01/01/1970 | Y |

| 71320 | 1,000,000.00 | 01/01/1970 | 12/07/2021 | 06/08/2021 | Y |

| 71334 | 2,000,000.00 | 03/01/2022 | 10/01/2022 | 01/01/1970 | Y |

| 71637 | 5,000,000.00 | 01/01/1970 | 05/05/2020 | 01/01/1970 | Y |

| 71862 | 500,000.00 | 08/07/2017 | 01/01/1970 | 01/01/1970 | Y |

| 71935 | 4,500,000.00 | 08/03/2021 | 11/03/2021 | 12/04/2021 | Y |

| 72264 | 2,000,000.00 | 12/06/2021 | 01/01/1970 | 01/01/1970 | Y |

| 72659 | 1,186,253.00 | 01/01/1970 | 07/05/2020 | 01/01/1970 | Y |

| 72678 | 750,000.00 | 01/01/1970 | 01/01/1970 | 05/01/2022 | Y |

| 72741 | 4,500,000.00 | 04/02/2021 | 01/01/1970 | 01/01/1970 | Y |

| 72764 | 5,000,000.00 | 01/01/1970 | 01/01/1970 | 09/02/2017 | Y |

| 72857 | 2,000,000.00 | 01/01/1970 | 03/04/2017 | 01/01/1970 | Y |

| 72876 | 7,000,000.00 | 01/01/1970 | 11/09/2020 | 05/11/2020 | Y |

| 73035 | 1,000,000.00 | 04/07/2019 | 01/01/1970 | 01/01/1970 | Y |

| 73135 | 1,500,000.00 | 03/08/2017 | 01/01/1970 | 01/01/1970 | Y |

| 73158 | 5,000,000.00 | 01/01/1970 | 01/01/1970 | 11/03/2019 | Y |

| 73165 | 10,000,000.00 | 09/07/2020 | 04/11/2020 | 11/03/2021 | Y |

| 73436 | 3,500,000.00 | 01/01/1970 | 01/01/1970 | 11/08/2020 | Y |

| 73596 | 500,000.00 | 01/01/1970 | 01/01/1970 | 01/04/2020 | Y |

| 73597 | 5,000,000.00 | 07/09/2020 | 07/12/2020 | 02/02/2021 | Y |

| 73663 | 5,000,000.00 | 11/10/2019 | 04/11/2019 | 01/01/1970 | Y |

| 73737 | 5,000,000.00 | 01/01/1970 | 01/01/1970 | 06/03/2017 | Y |

| 73772 | 2,000,000.00 | 01/01/1970 | 01/01/1970 | 01/01/1970 | Y |

| 73842 | 5,000,000.00 | 11/08/2021 | 12/08/2021 | 08/12/2021 | Y |

| 73864 | 2,000,000.00 | 04/04/2019 | 01/01/1970 | 07/06/2019 | Y |

| 73890 | 2,500,000.00 | 11/01/2022 | 11/01/2022 | 08/02/2022 | Y |

| 74562 | 1,000,000.00 | 01/01/1970 | 10/07/2017 | 01/01/1970 | Y |

| 74889 | 10,000,000.00 | 01/01/1970 | 01/01/1970 | 12/06/2018 | Y |

| 75021 | 5,000,000.00 | 01/01/1970 | 01/01/1970 | 11/08/2021 | Y |

| 75064 | 4,000,000.00 | 01/01/1970 | 02/03/2020 | 01/01/1970 | Y |

| 75075 | 5,000,000.00 | 01/01/1970 | 01/01/1970 | 12/09/2017 | Y |

| 75216 | 3,500,000.00 | 01/01/1970 | 01/01/1970 | 12/08/2020 | Y |

| 75291 | 3,000,000.00 | 01/01/1970 | 12/01/2017 | 01/01/1970 | Y |

| 75323 | 250,000.00 | 01/01/1970 | 01/01/1970 | 01/03/2017 | Y |

| 75347 | 800,000.00 | 12/06/2020 | 01/01/1970 | 01/01/1970 | Y |

| 75348 | 800,000.00 | 12/06/2020 | 01/01/1970 | 01/01/1970 | Y |

| 75349 | 700,000.00 | 12/06/2020 | 01/01/1970 | 01/01/1970 | Y |

| 75401 | 5,000,000.00 | 12/12/2018 | 01/01/1970 | 01/01/1970 | Y |

| 75433 | 10,000,000.00 | 10/09/2017 | 01/01/1970 | 01/01/1970 | Y |

| 75547 | 5,000,000.00 | 03/05/2019 | 06/05/2019 | 08/07/2019 | Y |

| 75548 | 5,000,000.00 | 03/05/2019 | 06/05/2019 | 08/07/2019 | Y |

| 75879 | 250,000.00 | 01/01/1970 | 07/06/2022 | 01/01/1970 | Y |

| 75905 | 5,000,000.00 | 08/04/2020 | 01/01/1970 | 01/01/1970 | Y |

| 76025 | 2,000,000.00 | 01/01/1970 | 01/01/1970 | 01/01/1970 | Y |

| 76066 | 1,079,000.00 | 01/01/1970 | 01/01/1970 | 09/02/2022 | Y |

| 76153 | 800,000.00 | 01/01/1970 | 04/12/2017 | 01/01/1970 | Y |

| 76250 | 3,000,000.00 | 08/04/2020 | 01/01/1970 | 12/05/2020 | Y |

| 76324 | 2,500,000.00 | 01/01/1970 | 08/01/2021 | 01/01/1970 | Y |

| 76340 | 5,000,000.00 | 01/01/1970 | 01/01/1970 | 01/01/1970 | Y |

| 76389 | 5,000,000.00 | 01/01/1970 | 01/01/1970 | 01/01/1970 | Y |

| 76403 | 2,422,306.62 | 01/01/1970 | 01/03/2019 | 01/01/1970 | Y |

| 76430 | 1,400,000.00 | 08/12/2020 | 01/01/1970 | 01/01/1970 | Y |

| 76511 | 5,000,000.00 | 01/01/1970 | 01/01/1970 | 01/01/1970 | Y |

| 76659 | 5,000,000.00 | 11/08/2021 | 12/08/2021 | 08/12/2021 | Y |

| 76963 | 2,000,000.00 | 01/01/1970 | 11/09/2020 | 01/01/1970 | Y |

| 76990 | 8,000,000.00 | 01/01/1970 | 01/01/1970 | 03/10/2019 | Y |

| 77038 | 1,000,000.00 | 01/01/1970 | 01/01/1970 | 01/01/1970 | Y |

| 77250 | 5,000,000.00 | 09/09/2017 | 01/01/1970 | 01/01/1970 | Y |

| 77261 | 5,000,000.00 | 01/01/1970 | 01/01/1970 | 01/01/1970 | Y |

| 77301 | 5,000,000.00 | 12/06/2019 | 01/01/1970 | 05/09/2019 | Y |

| 77418 | 4,000,000.00 | 12/12/2018 | 07/01/2019 | 07/02/2019 | Y |

| 77531 | 1,000,000.00 | 01/01/1970 | 01/01/1970 | 11/03/2022 | Y |

| 77753 | 5,000,000.00 | 01/01/1970 | 01/01/1970 | 01/01/1970 | Y |

| 77904 | 1,000,000.00 | 01/01/1970 | 10/11/2021 | 02/12/2021 | Y |

| 78006 | 2,500,000.00 | 01/01/1970 | 02/08/2018 | 01/01/1970 | Y |

| 78007 | 2,500,000.00 | 01/01/1970 | 02/08/2018 | 01/01/1970 | Y |

| 78008 | 2,500,000.00 | 01/01/1970 | 02/08/2018 | 04/09/2018 | Y |

| 78090 | 5,000,000.00 | 01/01/1970 | 01/01/1970 | 05/01/2021 | Y |

| 78280 | 500,000.00 | 01/01/1970 | 01/01/1970 | 01/01/1970 | Y |

| 78824 | 250,000.00 | 12/02/2018 | 10/03/2020 | 01/01/1970 | Y |

| 78830 | 1,500,000.00 | 01/01/1970 | 05/03/2019 | 05/04/2019 | Y |

| 78864 | 350,000.00 | 01/01/1970 | 01/01/1970 | 01/01/1970 | Y |

| 79190 | 500,000.00 | 01/01/1970 | 01/01/1970 | 01/01/1970 | Y |

| 79466 | 8,500,000.00 | 01/01/1970 | 01/01/1970 | 12/12/2019 | Y |

| 79625 | 4,750,000.00 | 01/01/1970 | 02/07/2019 | 01/01/1970 | Y |

| 79792 | 5,000,000.00 | 02/04/2020 | 06/04/2020 | 01/01/1970 | Y |

| 79849 | 3,000,000.00 | 12/01/2021 | 01/01/1970 | 01/01/1970 | Y |

| 80004 | 5,000,000.00 | 07/07/2017 | 01/01/1970 | 07/09/2017 | Y |

| 80278 | 900,000.00 | 11/12/2019 | 01/01/1970 | 01/01/1970 | Y |

| 80706 | 10,000,000.00 | 01/01/1970 | 12/03/2018 | 01/01/1970 | Y |

| 80756 | 7,250,000.00 | 09/05/2018 | 01/01/1970 | 01/01/1970 | Y |

| 80796 | 728,854.74 | 10/08/2019 | 01/01/1970 | 10/04/2020 | Y |

| 81116 | 2,000,000.00 | 01/01/1970 | 01/01/1970 | 01/01/1970 | Y |

| 81135 | 2,500,000.00 | 01/01/1970 | 01/01/1970 | 06/02/2020 | Y |

| 81177 | 3,000,000.00 | 01/01/1970 | 06/11/2017 | 01/01/1970 | Y |

| 81231 | 10,000,000.00 | 10/08/2019 | 01/01/1970 | 01/01/1970 | Y |

| 81287 | 1,885,573.25 | 01/01/1970 | 01/01/1970 | 01/01/1970 | Y |

| 81300 | 5,000,000.00 | 11/08/2021 | 12/08/2021 | 08/12/2021 | Y |

| 81387 | 3,000,000.00 | 01/01/1970 | 01/01/1970 | 01/01/1970 | Y |

| 81650 | 1,500,000.00 | 01/01/1970 | 01/01/1970 | 01/01/1970 | Y |

| 81861 | 3,000,000.00 | 01/01/1970 | 01/01/1970 | 01/01/1970 | Y |

| 82186 | 4,000,000.00 | 11/09/2017 | 01/01/1970 | 01/01/1970 | Y |

| 82212 | 846,403.27 | 01/01/1970 | 01/01/1970 | 01/01/1970 | Y |

| 82648 | 500,000.00 | 01/01/1970 | 02/10/2017 | 12/12/2017 | Y |

| 82649 | 1,000,000.00 | 01/01/1970 | 02/10/2017 | 12/12/2017 | Y |

| 82850 | 1,100,000.00 | 03/03/2018 | 01/01/1970 | 01/01/1970 | Y |

| 82919 | 2,000,000.00 | 03/03/2018 | 01/01/1970 | 01/01/1970 | Y |

| 82943 | 5,000,000.00 | 01/01/1970 | 01/01/1970 | 01/01/1970 | Y |

| 82962 | 3,000,000.00 | 01/01/1970 | 01/01/1970 | 01/01/1970 | Y |

| 83151 | 2,500,000.00 | 01/01/1970 | 10/03/2021 | 01/01/1970 | Y |

| 83447 | 4,000,000.00 | 01/01/1970 | 01/01/1970 | 12/11/2021 | Y |

| 83869 | 250,000.00 | 01/01/1970 | 07/06/2022 | 01/01/1970 | Y |

| 84232 | 100,000.00 | 01/01/1970 | 03/01/2017 | 09/03/2017 | Y |

| 84233 | 100,000.00 | 01/01/1970 | 03/01/2017 | 09/03/2017 | Y |

| 84480 | 5,000,000.00 | 07/01/2017 | 06/11/2017 | 10/04/2018 | Y |

| 85475 | 250,000.00 | 12/02/2018 | 10/03/2020 | 01/01/1970 | Y |

| 85491 | 3,000,000.00 | 01/01/1970 | 01/01/1970 | 01/01/1970 | Y |

| 86001 | 10,000,000.00 | 01/01/1970 | 12/04/2022 | 01/01/1970 | Y |

| 86269 | 1,000,000.00 | 01/01/1970 | 09/04/2019 | 01/01/1970 | Y |

| 86428 | 4,000,000.00 | 09/04/2020 | 06/05/2020 | 01/01/1970 | Y |

| 86513 | 10,000,000.00 | 01/01/1970 | 01/01/1970 | 09/07/2021 | Y |

| 86662 | 3,000,000.00 | 01/01/1970 | 01/01/1970 | 11/03/2019 | Y |

| 87174 | 2,000,000.00 | 12/08/2020 | 01/01/1970 | 01/01/1970 | Y |

| 88040 | 568,493.16 | 01/01/1970 | 01/01/1970 | 01/01/1970 | Y |

| 88041 | 568,496.13 | 01/01/1970 | 01/01/1970 | 01/01/1970 | Y |

| 88042 | 573,384.50 | 01/01/1970 | 01/01/1970 | 01/01/1970 | Y |

| 88043 | 573,666.49 | 01/01/1970 | 01/01/1970 | 01/01/1970 | Y |

| 88054 | 25,000.00 | 02/01/2019 | 01/01/1970 | 01/01/1970 | Y |

| 88369 | 42,000.00 | 01/01/1970 | 01/01/1970 | 01/01/1970 | Y |

| 88370 | 29,400.00 | 01/01/1970 | 01/01/1970 | 01/01/1970 | Y |

| 89993 | 304,300.00 | 01/01/1970 | 01/01/1970 | 03/05/2019 | Y |

| 90623 | 3,076,351.98 | 01/01/1970 | 12/08/2019 | 01/01/1970 | Y |

| 91030 | 10,000,000.00 | 01/01/1970 | 01/01/1970 | 01/01/1970 | Y |

| 91574 | 350,000.00 | 01/01/1970 | 01/01/1970 | 01/01/1970 | Y |

| 91579 | 2,000,000.00 | 12/12/2021 | 01/01/1970 | 01/01/1970 | Y |

| 91627 | 500,000.00 | 01/01/1970 | 01/01/1970 | 10/04/2018 | Y |

| 91628 | 350,000.00 | 11/03/2020 | 01/01/1970 | 01/01/1970 | Y |

| 91826 | 254,721.00 | 01/01/1970 | 01/01/1970 | 01/01/1970 | Y |

| 92750 | 37,700.00 | 01/01/1970 | 01/01/1970 | 01/01/1970 | Y |

| 92751 | 20,300.00 | 01/01/1970 | 01/01/1970 | 01/01/1970 | Y |